Here is simple guide to understanding back taxes and how tax relief can benefit you.

Tax Accountant, Tax Shark

According to the research conducted by CNN in 2016, approximately $458 billion in tax liability remains unpaid every year. Moreover, Investopedia indicates that just seven years before that, the cumulative amount of debt originating from back taxes was $83 billion.

Thus, it took less than a decade for it to increase by more than 5.5 times. While the tax law changes from 2017, which shifted the tax brackets and dropped tax rates, helped people get some additional refunds, the number of Americans who have to deal with unpaid taxes is still counted in millions.

The Internal Revenue Service, or the IRS, mandates all individuals to file and pay their federal income tax returns by April 15 of every year. While there is some flexibility with the filling portion of the law, you must pay what you owe by the said date. In other words, getting an extension does not grant you the right to pay at a later time.

Well, if you have ever failed to eliminate your tax liability by April 15, you effectively created “back taxes” that the IRS will deem late and start enforcing penalties and fees upon. The longer that you wait to pay them, the higher the fees will be. Hence why it is imperative that you submit your tax return and any accompanying payment in timely fashion.

Unfortunately, countless Americans find themselves in unpredictable situations where they are unable to pay their taxes due to various life events. Given how quickly this debt can snowball, it is not surprising to see it build up to tens of thousands of dollars payable to one of this nation’s strictest and least forgiving agencies, the IRS.

Luckily, there are multiple ways that you can go about eliminating your back taxes in a way that will not leave you completely insolvent. To understand some of the basic approaches, consider the following methods.

Payment plans offered by the IRS are amongst the most popular solutions to overcoming tax debt in a way that does not force you into bankruptcy. Currently, there are only two alternatives that you can choose from when it comes to the type of plan that you want – the short- and long-term one. The short-term plan will give you no more than approximately four months or 120 days to pay everything off while the long-term plan lets you pay over a period of more than 120 days.

Outside of the timeframe, the main difference between the two is the setup fee and the available payment options. The short-term plan does not cost anything to set up and allows you to pay via direct pay, electronically, or by check, and the long-term plan can cost up to $225 but offers a slew of payment options.

The detailed breakdown provided by the IRS is depicted below. Do not forget, however, that entering a payment plan will have no impact on your penalties and fees as those continue to accrue until the entirety of the debt is eliminated.

| Payment Method | Costs |

|---|---|

After applying for a short-term payment plan, payment options include:

|

|

| Payment Options | Costs |

|---|---|

|

Option 1: Pay through Direct Debit (automatic monthly payments from your checking account). Also known as a Direct Debit Installment Agreement (DDIA). |

|

|

Option 2: After applying for a long-term payment plan, payment options include:

|

|

While the payment plan works for millions of Americans who struggle with tax settlement, there are many situations where someone simply finds themselves unable to make any payments whatsoever. Common examples would include individuals who have undergone medical issues that have rendered them unable to work and generate income needed to cover the monthly payments.

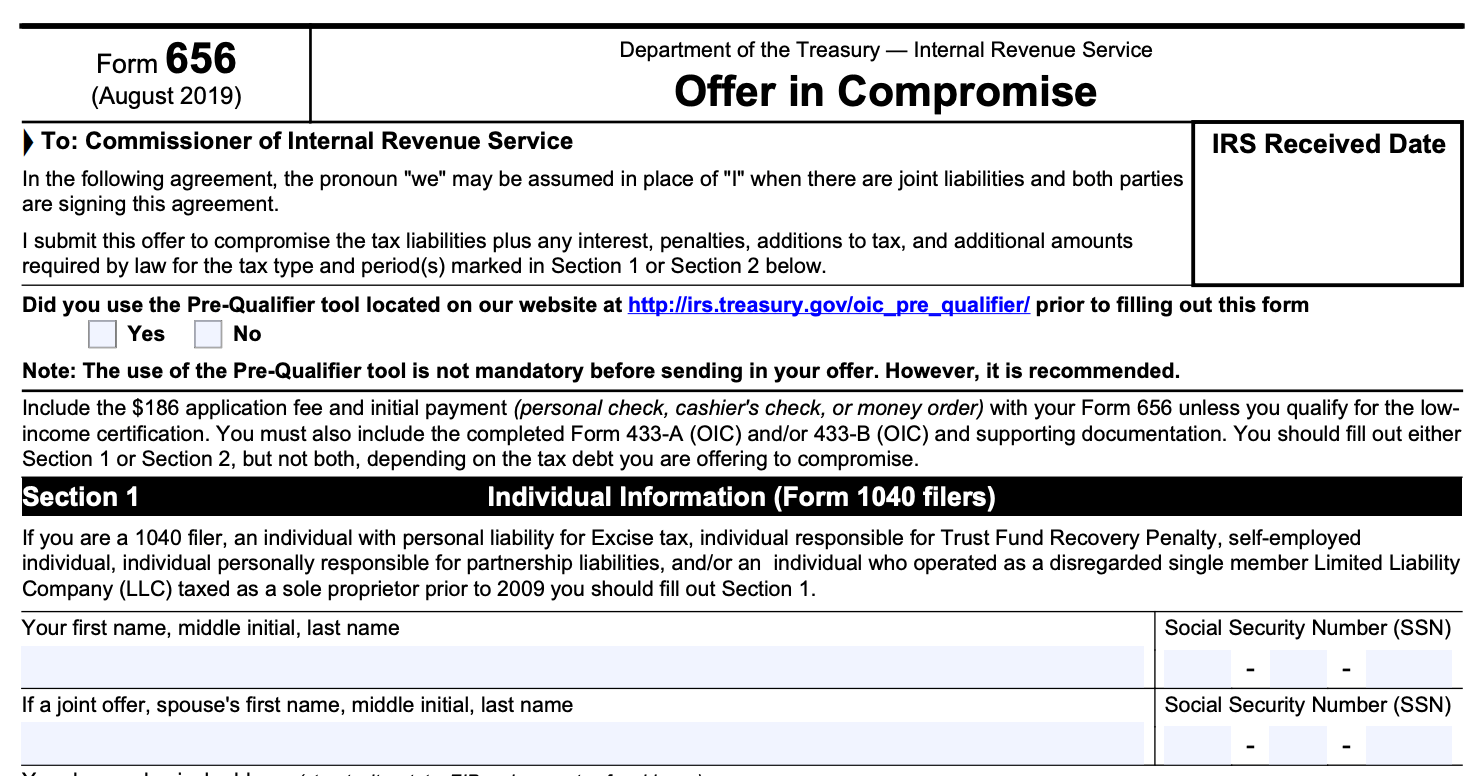

In those situations, the IRS allows for something known as the “Offer in Compromise.” This method begins by you filing Form 656-B, which is depicted below, where you are submitting the offer that you would like the IRS to consider in lieu of the current debt.

Instead of paying the full amount, you are offering to pay only a portion of it due to your extenuating circumstances. Unlike the aforementioned solution, however, the offer in compromise comes with a lengthy list of eligibility criteria that you must satisfy.

Examples include not having an open bankruptcy, being current on all tax returns, and making an initial payment alongside the non-refundable $186 fee. You should also keep in mind that whilst payment plan applications are almost turning into a mere formality for qualifying individuals, given that the IRS accepts most of them, offers in compromise are a lot harder to get by.

The agency accepts less than half of all offers sent to them as every situation is analyzed on a case-by-case basis using a high level of subjectivity. If approved, remember that any outstanding tax liens or penalties will not be eliminated until the entire debt is gone.

If you are in a situation where you cannot pay your back taxes but have not been long-term disabled and anticipate getting back on your feet, you may want to think about taking a temporary delay. This is known as the “Currently Not Collectible” account status that you can request from the IRS. Unlike the previous solution, it does not reduce the liability; it simply puts a pause on the account which usually prevents the IRS from filing a tax lien against you or garnishing your wages.

This is something that you should keep as one of the last options that you go to as it is by no means a solution to the problem, it is just a temporary fix that repairs a minor leak during a major flood. The IRS will continue to monitor your status and follow up through your annual returns to see if you have started earning the necessary income; they can also file a tax lien at any point as the “currently not collectible” status does not legally prevent them from doing so.

Since interacting with the IRS can be an extremely overwhelming process, there is a large market of providers who help people resolve their tax issues. These include companies that specialize in representing or working with someone who has issues related to back taxes, failures to file, and similar. In fact, hiring a tax relief service is something that can help you accurately determine if you should attempt the payment plan, offer in compromise, or a temporary delay route. So, how exactly does it work?

The first thing that you should recognize is that tax attorneys are not going to be able to momentarily eliminate any of your debt. As with every other legal process, there is a strict timeline that must be followed.

Nonetheless, having a certified public accountant or a Bar-certified lawyer in your corner is going to make it much less likely that you fail to submit an important document or miss a deadline. These individuals will also be able to leverage their own experience and track record to your benefit and advise you on the most fitting strategy given the size of your outstanding debt and life circumstances.

Note that this is a fee-for-service option as the experts that handle your case have to put in the necessary hours to achieve a favorable outcome.

The specific costs can be hard to narrow down, though, as each case is approached on an individual basis and depends on someone’s situation. This is why it is imperative that you start your research early and focus on companies who have a good business history and positive customer reviews.

Doing so could help you sidestep a lot of issues that the IRS can bring your way once they file a tax lien against you or start taking money directly from your paychecks through wage garnishment.

Lana from Tax Shark was able to answer all of my questions and help me with my situation. She did the research on my issue and got it taken care of. Don't neglect your taxes boys and girls.

Jon E. - Contractor